Regardless of type, size or administrative budget, timely and accurate financial reporting plays a vital role in determining whether a nonprofit can fulfill https://www.bookstime.com/ its mission. Financial statements that contain accounting errors can undermine both the long-term and short-term viability of an organization.

The Accounting errors happens in entering the transactions in journal or subsidiary books or at the time of posting of entries in to the ledger. The accounting errors may happen because of the omission, commission, principle or as a compensating of errors. Lastly, you have to correct the error on each of the comparative-year financial statements. Your intermediate accounting textbook may refer to this as period-specific effects.

What are the different types of errors?

There are three types of error: syntax errors, logical errors and run-time errors. (Logical errors are also called semantic errors). We discussed syntax errors in our note on data type errors. Generally errors are classified into three types: systematic errors, random errors and blunders.

When an error is committed in the books of accounts the same should be corrected to show true numbers in financial statements. If the error is immediately identified it may be fixed by striking out the wrong entry and replacing it with a correct one. However, if the error is identified at types of errors in accounting a later stage, the correction should be made by passing a suitable journal entry, such entries used to fix an accounting error are called rectification entries. If a journal entry is created where the debit and credit totals are not the same, this is called an unbalanced journal entry.

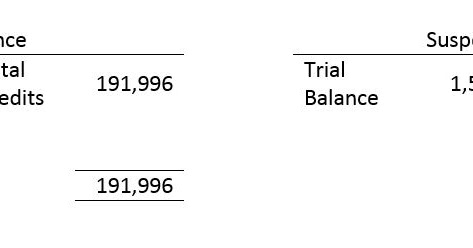

If you attempt to enter an unbalanced journal entry into a computer accounting system, the error-checking controls in the software will likely reject the entry. However, if you create an unbalanced journal entry in a manual accounting system, the result will be an unbalanced trial balance, which in turn means that the balance sheet will not balance.

Like other professionals, bookkeepers and accountants can make mistakes. The difference is that these mistakes might direct you and your company to make the wrong business decisions and have you headed in the wrong direction.

Correcting entries are part of the accrual accounting system, which uses double-entry bookkeeping. This means the correcting entry will have both a debit and a credit. Many accounting errors can be identified by checking your trial balance and/or performing reconciliations, such as comparing your accounting records to your bank statement. https://www.bookstime.com/articles/accounting-errors When we cannot locate and rectify the errors before the final accounts, we need to carry forward the balance of the Suspense A/c to the next financial year. When we rectify the errors of the previous accounting year, we need to route them through the Profit and Loss Adjustment A/c for the items of expenses, losses, incomes and gains.

Accounting mistakes can keep your small business from running smoothly and hurt growth so it’s important to learn the common types of accounting errors and how to correct them. The best way to correct errors in accounting is to add a correcting entry. A correcting entry normal balance is a journal entry used to correct a previous mistake. All data entries must be classified as assets (items owned) or liabilities (money owed). If an asset is accidentally entered as an expense (a type of liability), then it is said to be classified incorrectly.

Similarly, we can also correct an error in the ledger account. Opening entries are those entries which record the balances of assets and liabilities, including capital brought forward, from a previous accounting period. In the case of going concerns, there is always a possibility of having balances of assets and liabilities, including capital, which were lying in the previous accounting year. To show true and fair view of the business concern, it is necessary that all previous balances are to be brought forward in the next year by way of passing an opening entry.

These types of errors require lots of time and resources to find and correct them. It is useful for constructing trend lines to examine the relative changes in the size of different accounts. This format presents information about an entity’s assets, liabilities, and shareholders‘ equity that is aggregated (or „classified“) into subcategories of accounts. It is the most common type of balance sheet presentation, and does a good job of consolidating a large number of individual accounts into a format that is eminently readable. Accountants should present balance sheet information in the same classification structure over multiple periods, to make the information in the periods more comparable.

The accounting errors will hardly affect the accuracy of trial balance of the business because the trial balance is the final proof of the books of accounts. There are some of the methods to rectify the accounting errors happened in the books of accounts. bookkeeping The important two methods for rectifying the accounting errors are as follow. Accounting errors are those mistakes which occurs in the book keeping or accounting, relating to a routine activity or relating to the principle of accounting.

- When an error is committed in the books of accounts the same should be corrected to show true numbers in financial statements.

- If the error is immediately identified it may be fixed by striking out the wrong entry and replacing it with a correct one.

Balance sheets are easy to do if you use accounting software. Accounting software designed for small businesses can keep track of all your accounting information and generate balance sheets, cash flow statements, and other reports automatically as needed. A balance sheet is a statement of the financial position of a business that lists the assets, liabilities, and owner’s equity at a particular point in time. In other words, the balance sheet illustrates your business’s net worth. A journal is also named the book of original entry, from when transactions were written in a journal prior to manually posting them to the accounts in the general ledger or subsidiary ledger.

What are the different types of error in accounting?

The most common (with simple examples): Error of omission: an accounts payable account is not credited when goods are purchased on credit. Error of commission: an account receivable is credited to the wrong customer. Error of original entry: the wrong amount is posted to an account.

Types of Errors in Accounting: A Guide for Small Businesses

The following journal entry is unbalanced; note that the debit total is less than the credit total. In such cases, you must correct the underlying unbalanced journal entry before you can issue financial statements.

There are some errors, which effect Trading or Profit and Loss account and Balance sheet simultaneously, like entry of depreciation will affect profit as well as value of the Fixed Assets. Financial accounting deals with recording and maintaining every monetary transaction of an organization.

Errors of Principle

However, sometimes, a few entries might be either incorrect or used at the wrong place. In financial accounting, the process of correcting such mistakes is known as Rectification of Errors. Errors can either be small mistakes that don’t affect the overall figures or ones that snowball into greater miscalculations and need more time and resources to identify and repair.

Adding a journal entry may be enough to correct an accounting error. This type of journal entry is called a “correcting entry.” Correcting entries adjust an accounting period’s retained earnings i.e. your profit minus expenses.

This guide will teach you to perform financial statement analysis of the income statement, balance sheet, and cash flow statement including margins, ratios, growth, liquiditiy, leverage, rates of return and profitability. We can rectify these errors by giving an explanatory note in the account or by passing a journal entry with the help of Suspense A/c. When we detect an error before posting to the ledger, we can correct it by simply crossing the wrong amount, writing the correct amount above it and initializing it.

This error drastically affects the balance sheet and gives an incorrect picture of the business’s financial status. Small accounting online bookkeeping errors may not affect the final numbers in financial statements. Or they might cause major distortions in the overall figures.

We can rectify these by passing a journal entry giving the correct debit and credit to the accounts. In order to rectify an error, we need to cancel the effect of wrong debit or credit by reversing it and restore the effect of correct debit or credit. An accounting journal entry is the method used to enter an accounting transaction into the accounting records of a business. The accounting records are aggregated into the general ledger, or the journal entries may be recorded in a variety of sub-ledgers, which are later rolled up into the general ledger. This information is then used to construct financial statements as of the end of a reporting period.

Errors of Commission

Manual systems usually had a variety of journals such as a sales journal, purchases journal, cash receipts journal, cash disbursements journal, and a general journal. Depending on the business’s accounting information system, specialized journals may be used in conjunction with the general journal for record-keeping.